There are several different credit scoring models. However, more than 90% of creditors use the FICO score. Therefore, it is vital to know and understand your score.

A credit score is a 3-digit number used by creditors to determine a consumer’s credit risk. Your credit score can affect your ability to obtain a mortgage, credit card, or auto loan. Your credit rating will affect the terms offered to you for auto and home insurance.

The FICO Score is a credit score that the Fair Isaac Corporation created in 1989. Since its introduction, the FICO scoring model has been modified several times. Their goal is to provide creditors with the most valuable assessment of a consumer’s credit risk.

The FICO Score Range

| FICO Score Range | Credit Rating | Description |

| Less than 580 | Poor Credit | Well Below Average compared to other U.S. consumers |

| 580 – 669 | Fair Credit | Below Average compared to other U.S. consumers |

| 670 – 739 | Good Credit | Near or Slightly above average compared to other U.S. consumers |

| 740 – 799 | Very Good Credit | Above average compared to other U.S. consumers |

| 800 + | Exceptional | Well Above average compared to other U.S. consumers |

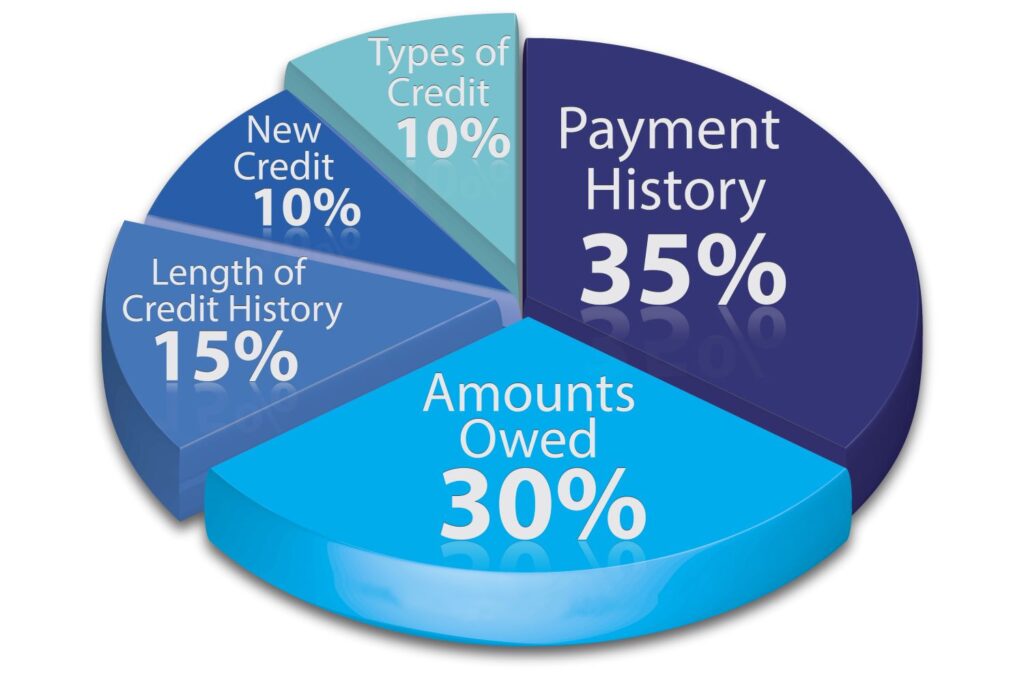

Factors That Impact your Score

The chart below shows the impact certain information on your credit report will have on your overall credit score.

Where to Obtain Your Score

You should always obtain your credit score directly from the source. MyFico.com allows you to purchase several versions of your FICO Score on their website.

There is a charge to obtain your credit score from MyFico.com. However, it is worth the cost to get your actual FICO Score, and not a knock-off version.

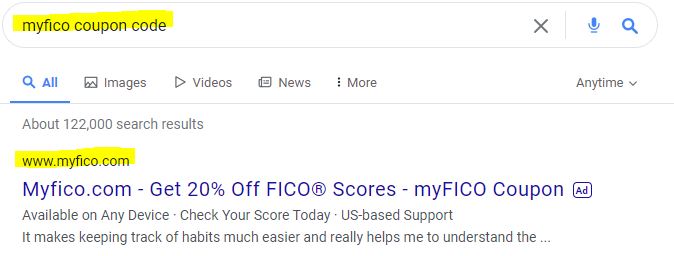

You can often get a discount by googling “myfico coupon code”. See the example below.

Avoid going to “coupon code” websites, as they often have expired codes. I have used the method above many times, and I have never had to pay full price for my credit score from myfico.com.

Different Versions of the Same Score

Did you know that there are multiple versions of the FICO Score?

Since creditors often use different information to determine your risk for certain types of credit, Fair Isaac has created several FICO Scores. There is a version used by mortgage lenders, a version most used by credit card lenders, and a version used by auto lenders.

I have personally compared the scores received on myfico.com to those obtained in credit disclosures from potential lenders during the same period, and they match.

When you obtain your credit scores from myfico.com, you will receive access to each of these versions of your score.

Learn how I increased my credit score to 800!

{kind=link}