Credit cards are great for establishing credit or improving your credit over time.

However, if you do not understand how credit cards work, you may find yourself hurting your credit instead of helping it.

I recently wrote an article entitled “4 Things I Wish Someone Told me About Credit Cards“. In that article, I pointed out that you should avoid using more than 10% of your credit limit.

Using more than 10% of your credit limit will signify to creditors that you are a risky consumer. However, there is a way to bypass this 10% rule and still make the creditors happy.

The Date More Important Than Your Due Date

You should always know the due dates for your bills. Your credit card is no exception to this rule. However, in addition to the due date, you should also be aware of your statement date.

Your credit card company may refer to this date as the “Closing Date” or the “Statement Cutoff Date”. No matter the name, the statement date is significant. Your statement date tells you when the credit card company reports balance information to the credit bureaus.

That’s right! The balance of your credit card is pretty insignificant 99% of the month. As long as you have paid the balance down to less than 10% by the statement closing date, you will have met the 10% rule.

Where Do You Find Your Statement Date?

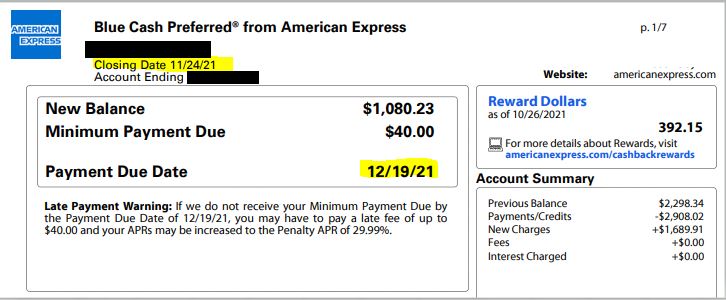

In the screen capture below, you can see my American Express credit card’s closing date and the due date.

You can see the payment for this credit card is due on December 19, 2021. However, the Closing Date for the statement was November 24.

If you look at your statement history, you will find that the statement date is generally around the same day each month.

How the Statement Date Affects Your Credit

As I already mentioned, the statement date is the date the credit card company reports your balance to the credit bureaus.

Based on my AMEX statement history, I expect that my next statement will be issued on the 24th of December. This means that there is a four-day lag between my due date and the next statement closing date.

Even if I paid the balance down to 0.00 by the due date, I may wipe out any benefit by making new charges to the card just before the statement closing date.

In my case, some last minute Christmas shopping on December 23rd could reduce my score if I ended up charging more than the last reported balance.

Therefore, understanding the importance of the statement date will help you to avoid adverse effects to your credit score. You are able to time your balances so that you have greater control over the information being reported.

{kind=link}